How to Purchase an Investment Property

This is part three of my investor series, if you interested in investing in real estate but don’t know where to start, this post may be for you! My first and second posts covered setting up an LLC and how to establish a business bank account and structure your accounts to efficiently manage your business finances. It’s important to handle this early on because when the money starts rolling in, you’ll want to have your systems in place to keep you on track for success!

As a Realtor in the Hampton Roads area of Virginia, I have helped many people purchase and sell homes and investment properties! I work closely with many great local lenders in the area, one being my friend Miles, with Southern Trust Mortgage. We’ve partnered up on this post to give you more information on how to purchase your first investment property!

There are many different loan types and lender qualifications, here are four safe ways to finance an investment property.

Conventional

A conventional mortgages for investment properties require 15%-25% down. The perk of this mortgage is that you can use it for an investment property and the PMI will fall off once the home has 20% equity! For a one unit investment property, the downpayment would be 15%, for 2-4 units it would be 25% down.

VA

**Disclaimer VA Loans are intended to be used for primary residences, however, the guidelines will allow a borrower to live in a multi unit property as their primary residence and rent out other units**

The VA loan is a great mortgage type for our Military service members, veterans and surviving spouses. With this loan the borrower can put 0% down and finance a home they plan to live in with no monthly mortgage fee. The VA allows a borrower to purchase a property with up to four units, meaning you can rent out the other three units and live in one. The VA is similar to FHA in the fact that they will consider 75% of the projected rental income for the additional units. If you purchase a single family home as a VA, you may rent the home if you purchase a new home. The VA does charge a funding fee but waives for the following per the VA website:

You won’t have to pay a VA funding fee if any of the below descriptions is true. You’re:

- Receiving VA compensation for a service-connected disability, or

- Eligible to receive VA compensation for a service-connected disability, but you’re receiving retirement or active-duty pay instead, or

- The surviving spouse of a Veteran who died in service or from a service-connected disability, or who was totally disabled, and you’re receiving Dependency and Indemnity Compensation (DIC), or

- A service member with a proposed or memorandum rating, before the loan closing date, saying you’re eligible to get compensation because of a pre-discharge claim, or

- A service member on active duty who before or on the loan closing date provides evidence of having received the Purple Heart

The funding fee is 2.3% for less than 5% down for first use and 3.6% for subsequent usage.

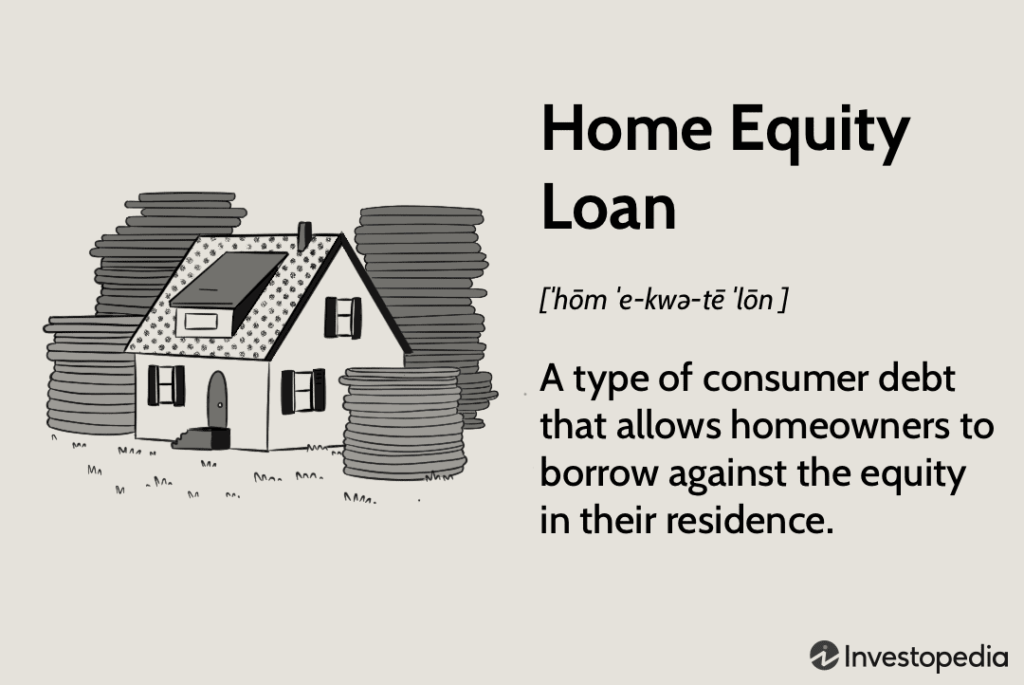

Cash out refinance or Home equity

A cash out refinance or a home equity may be a good option if you currently own a home or rental property with a lot of equity. Equity is the value of the home minus the balance on the mortgage. This would allow you to tap into the equity your home has earned and use it to purchase a new home or use toward a downpayment, repairs and updates.

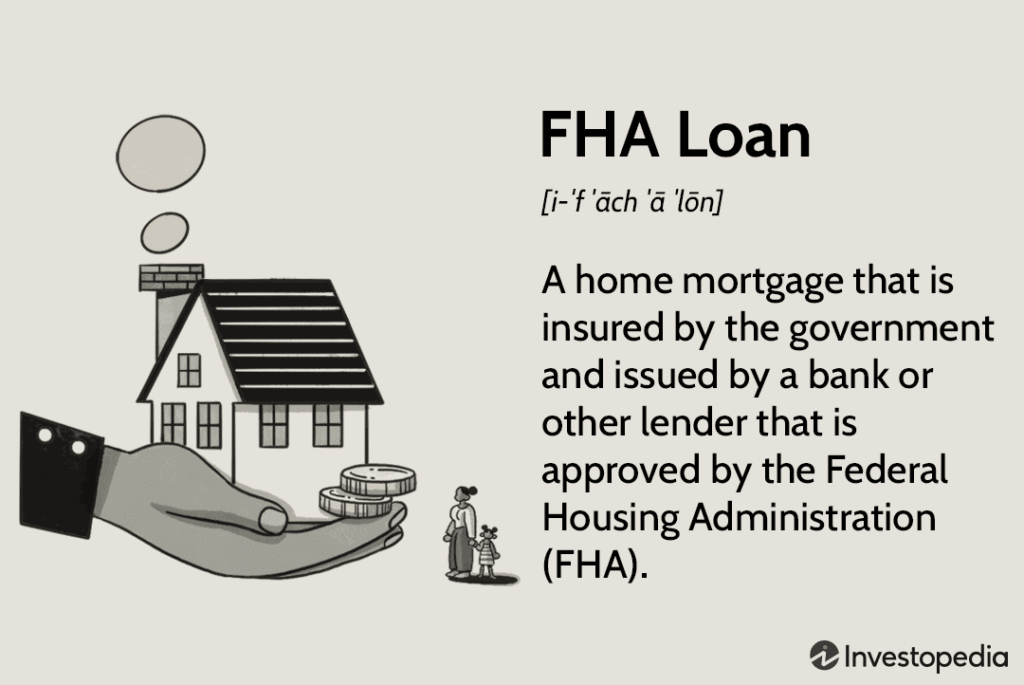

FHA

**Disclaimer FHA loans are intended to be used for primary residences, however, the guidelines will allow a borrower to live in a multi unit property as their primary residence and rent out other units**

FHA is a government backed loan that requires a minimum downpayment of 3.5%. When going this route, a borrower must live in the home for a year before renting the property out. If you are financing a 2-4 unit property, as long as you live in one of the units, FHA guidelines will allow you to use 75% of the projected rental income of the other units towards your monthly debt to income, meaning you may be able to qualify to borrow more money. The drawback with FHA loans is that it has an upfront mortgage insurance that gets financed into the loan amount as well as a monthly mortgage Insurance factored into the payment. This insurance is charged by the lender to the borrower to mitigate financial loss in the event the home is foreclosed on. This is an added expense either built into the loan amount or monthly payment that protects the lender and not the borrower. Even if the borrower puts 20% down, they will still be subject to mortgage insurance .

If you aren’t sure what loan type is the best for you, a lender will be able to asses your financial situation and go over the best options for you! For more information you can reach out to me directly or Miles at Southern Trust mortgage!

Now that we’ve covered how to finance an investment property, let’s go over how to determine what investment type is best for you! https://kristenmehne.com/what-you-need-to-know-about-buying-an-investment-property/